Sarasota Housing Market Spring 2026: What the Data Actually Says (And Why It Matters If You're Relocating)

Darren Dowling

Darren Dowling

If you've been following national real estate headlines lately, you might be tempted to hit pause on your plans to move to Sarasota. Affordability stress. Geopolitical uncertainty. Buyers sitting on the sidelines.

Here's the thing: national narratives are blunt instruments. Sarasota isn't Orlando. It isn't Phoenix. And it certainly isn't Austin.

The latest hard data, from Florida Realtors' SunStats (https://sunstats.floridarealtors.org/) for Sarasota County and the John Burns Real Estate Agent Survey (https://www.jbrec.com) (April 2026, data through March 2026), tells a story that's meaningfully different from the national one. For buyers considering a Gulf Coast relocation, that distinction is worth understanding.

Let's dig in.

The John Burns Real Estate Agent Survey polled approximately 800 resale agents nationwide for March 2026. Their headline findings:

This is the environment your friends in Chicago, New York, and Michigan are hearing about. And broadly, it's accurate, for most of the country.

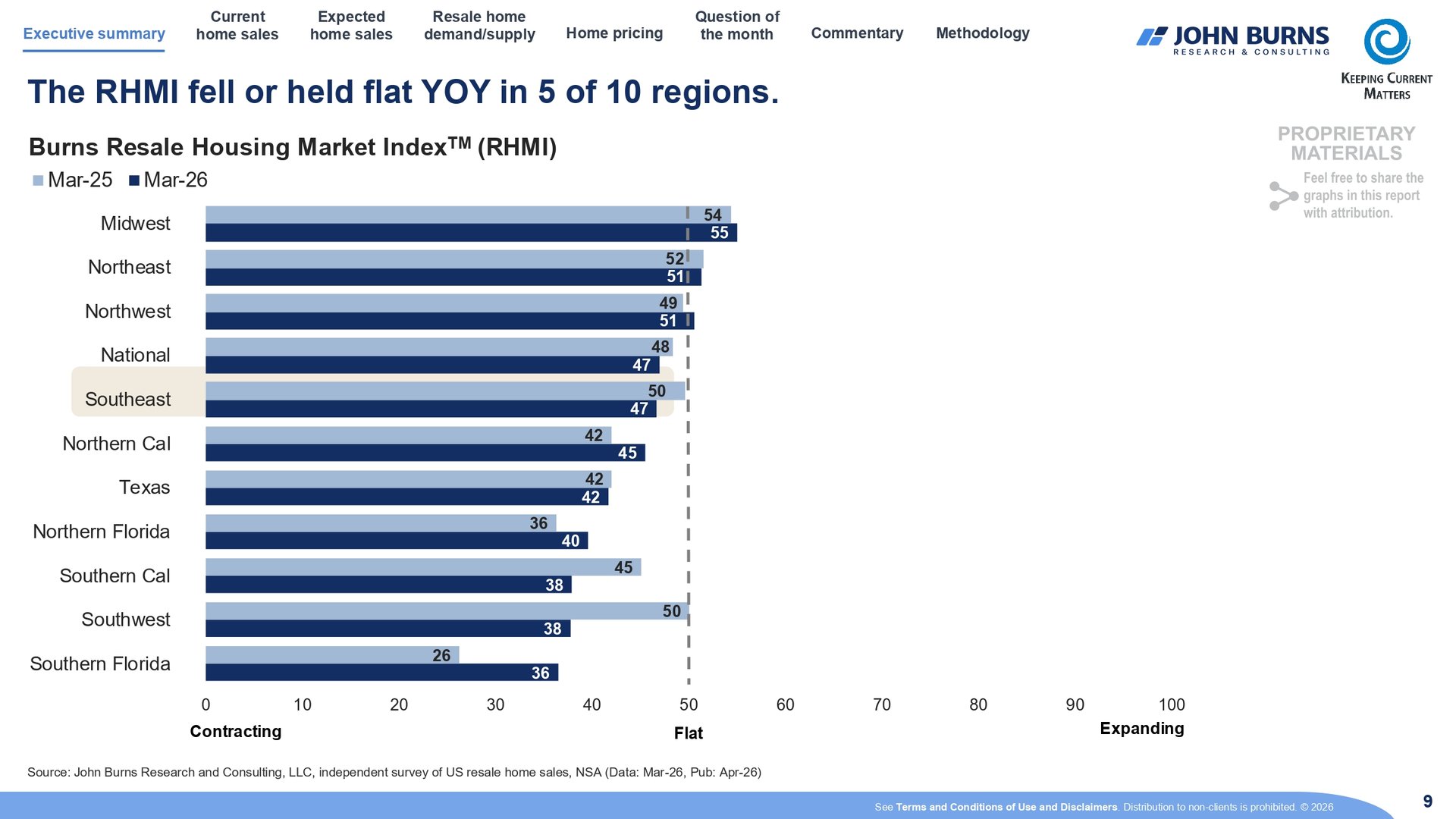

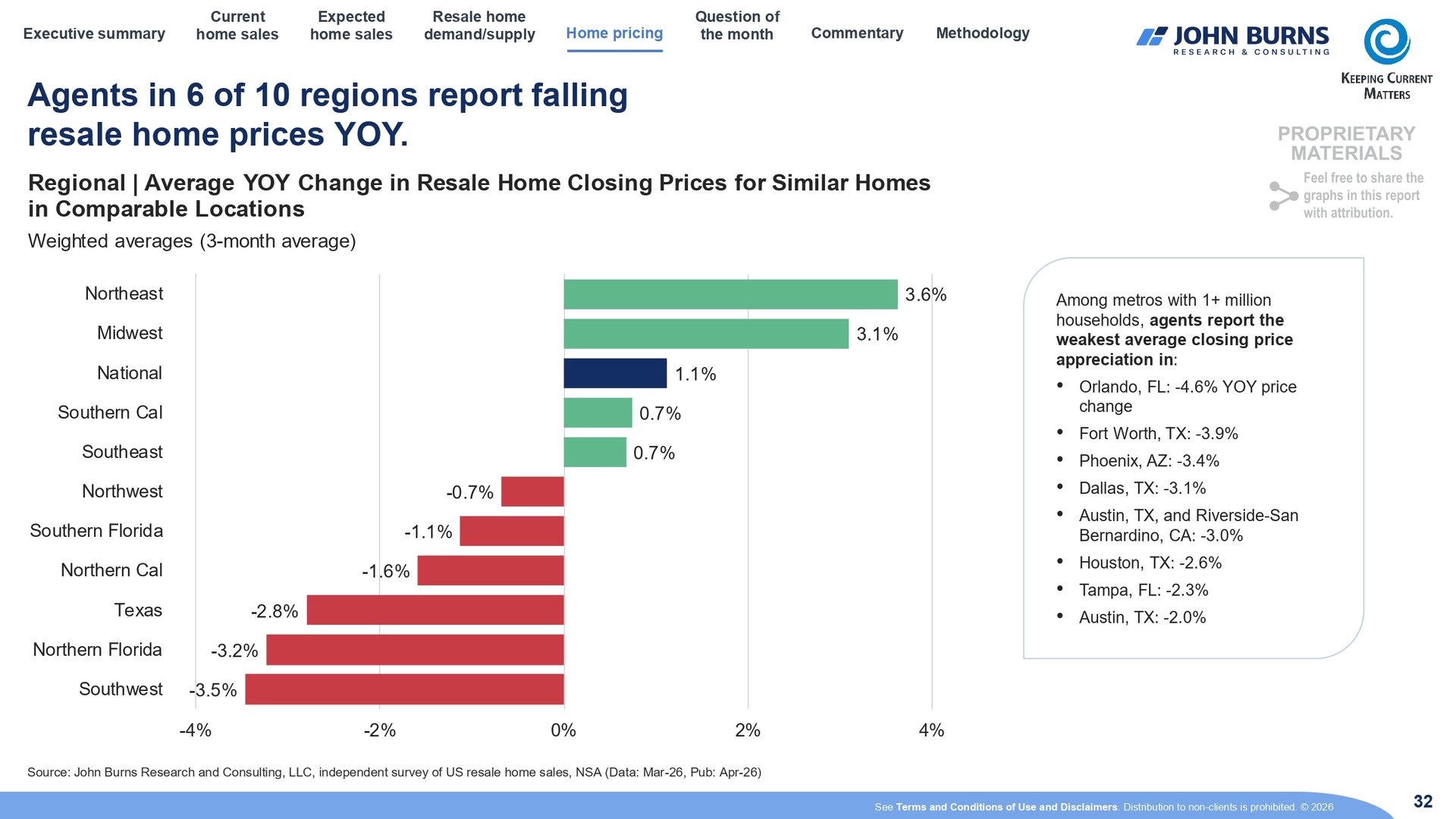

Within the national data, Southern Florida (which includes the Sarasota/Naples corridor) sits at a RHMI of 36, below the national average of 47, but importantly, up sharply from 26 just one year ago. That's a meaningful improvement in underlying market health.

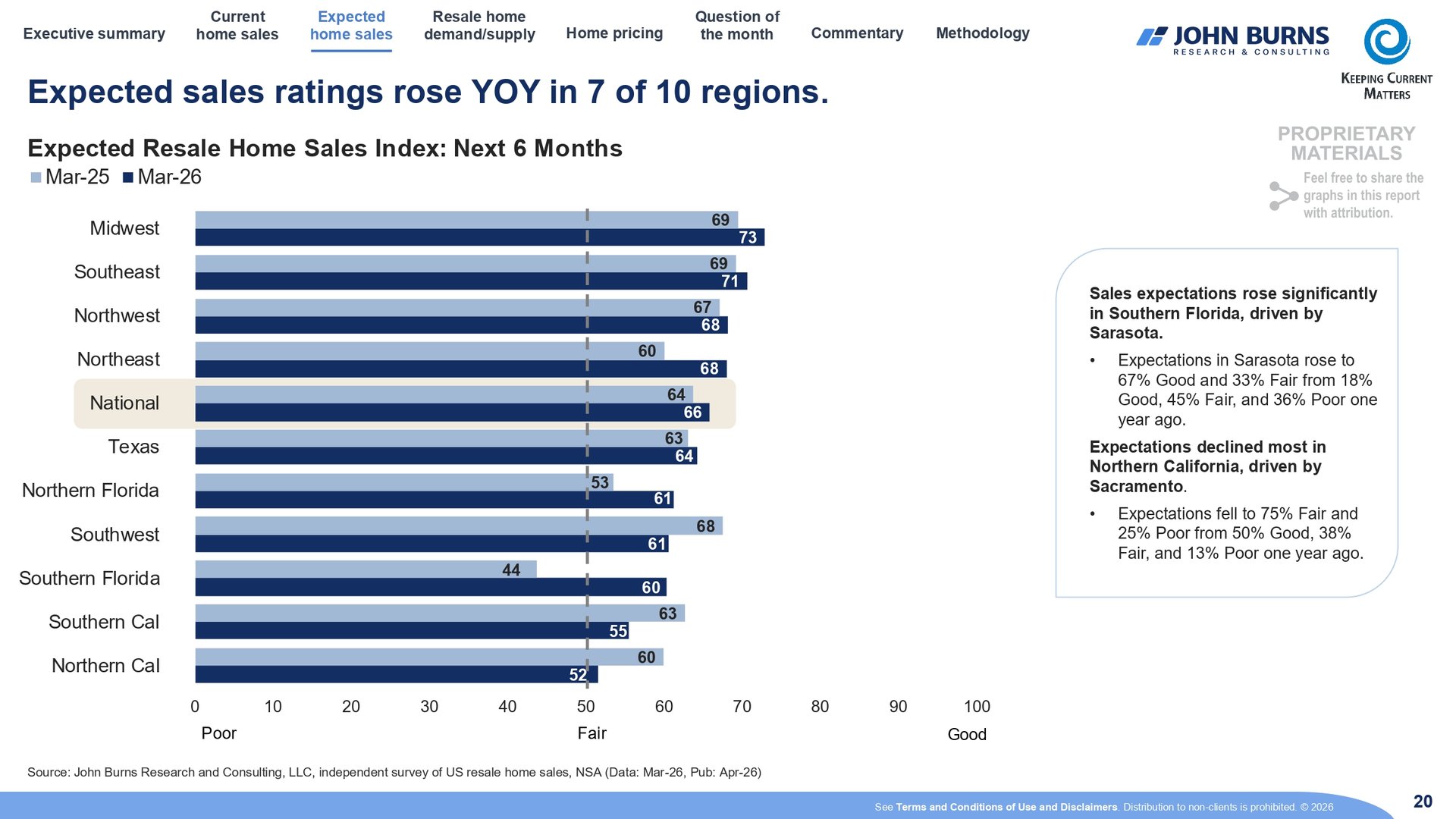

A few specific Sarasota callouts from the John Burns commentary section:

"Sales expectations in Sarasota rose to 67% Good and 33% Fair for the next six months, compared to just 18% Good, 45% Fair, and 36% Poor one year ago."

That is one of the largest single-year improvements in forward-looking agent sentiment recorded in the entire national survey. Agents on the ground in Sarasota are noticeably more optimistic about the second half of 2026 than they were this time last year.

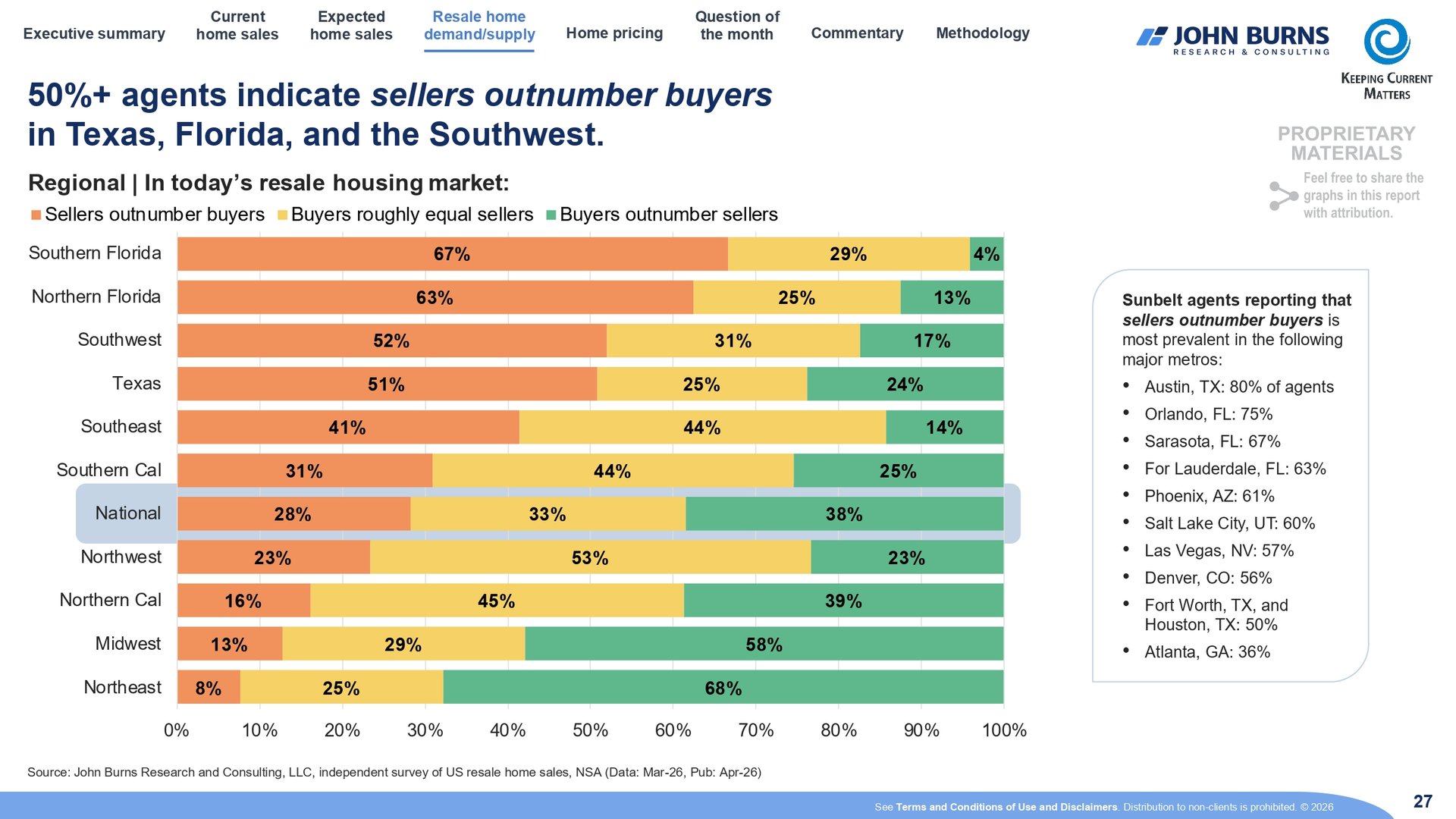

The survey also notes that 67% of Sarasota-area agents report sellers outnumber buyers in today's market, which is a supply reality, yes. But paired with the forward sentiment data, it tells a more nuanced story: buyers have leverage today, while agents expect conditions to tighten as the year progresses.

Here's where the local SunStats data gets genuinely interesting for anyone watching this market closely. These are single-family home statistics for Sarasota County, March 2026 vs. March 2025:

|

Metric |

Mar 2026 |

Mar 2025 |

Change |

|

Closed Sales |

890 |

817 |

+8.9% |

|

Cash Sales |

374 |

365 |

+2.5% |

|

Cash Sales as % of Closed |

42.0% |

44.7% |

-6.0% |

|

Median Sale Price |

$485,000 |

$469,450 |

+3.3% |

|

Average Sale Price |

$706,388 |

$727,555 |

-2.9% |

|

Dollar Volume |

$628.7M |

$594.4M |

+5.8% |

|

Median % of Original List Price |

93.8% |

94.2% |

-0.4% |

|

Median Time to Contract |

49 Days |

40 Days |

+22.5% |

|

Median Time to Sale |

88 Days |

82 Days |

+7.3% |

|

New Pending Sales |

895 |

837 |

+6.9% |

|

New Listings |

998 |

1,226 |

-18.6% |

|

Pending Inventory |

1,087 |

1,051 |

+3.4% |

|

Active Inventory |

3,351 |

4,412 |

-24.0% |

|

Months Supply of Inventory |

4.8 |

6.9 |

-30.4% |

Source: Florida Realtors SunStats (https://sunstats.floridarealtors.org/), Sarasota County Single-Family Homes, March 2026

Note: John Burns regional data for Southern Florida shows -1.1% YOY. Sarasota County's local SunStats data shows median prices up +3.3%, demonstrating that county-level data tells a more accurate story for Sarasota specifically.

Active inventory dropped from 4,412 homes to 3,351, a 24% decline year over year. Months supply fell from 6.9 to 4.8, a 30% reduction. This is the single most important structural shift in the Sarasota market over the past 12 months.

A year ago, Sarasota was a buyer's market by every textbook definition (anything above 6 months supply). Today, at 4.8 months, it's approaching balanced territory. If the trend continues, and fewer new listings coming to market (-18.6% YOY) suggests it will, we could see conditions tighten meaningfully by late 2026.

Closed sales rose 8.9% year over year. New pending sales rose 6.9%. Dollar volume rose 5.8%. These are not the numbers of a market in distress. Buyers are transacting, just more selectively and at a more deliberate pace than during the 2021-2022 frenzy.

The median sale price rose 3.3% year over year to $485,000, while the average sale price dipped 2.9% to $706,388. This divergence is important: it suggests that the upper end of the market (high-value luxury homes) saw some price compression, while the core mid-market held firm and appreciated.

For buyers targeting the $500K to $2M range, the primary sweet spot for most Gulf Coast relocators, the median data is the more relevant signal.

Homes are closing at 93.8% of original list price, down only slightly from 94.2% a year ago. Median time to contract stretched from 40 to 49 days. This tells you buyers have room to negotiate, but sellers aren't capitulating. Well-priced, well-presented homes are still selling. The gap is largely concentrated in overpriced or under-prepared listings.

This aligns directly with the John Burns national finding that agents increasingly report sellers with unrealistic price expectations are the primary drag, not a lack of buyers.

42% of all closed single-family home sales in Sarasota County were cash purchases in March 2026. This is consistent with the buyer profile we see most often: financially established professionals and retirees relocating from high-cost, high-tax states who are either selling a primary residence up north or drawing from liquid assets.

For financed buyers, this is worth understanding: you will compete against cash. A strong pre-approval and a clean offer structure matter more here than in most markets.

This is genuinely the best buying window Sarasota has offered in several years. You have:

• More inventory to choose from than at any point since 2020

• More negotiating room on price (sellers are closing at 93.8% of list on average)

• Longer time to conduct due diligence (49-day median time to contract)

• A market where sellers are increasingly motivated

The catch: that window may not stay open indefinitely. With inventory declining 24% YOY and fewer new listings coming to market, the next 6 to 12 months could look meaningfully different.

If you've been watching the market from afar, this is the data that should move you from observer to active participant. Learn more about our buyer representation process here.

Pricing accuracy and presentation are doing more work than ever. Agents nationwide, and specifically in Florida, are consistently reporting that sellers with outdated price expectations are sitting on the market while correctly priced, well-presented homes are moving.

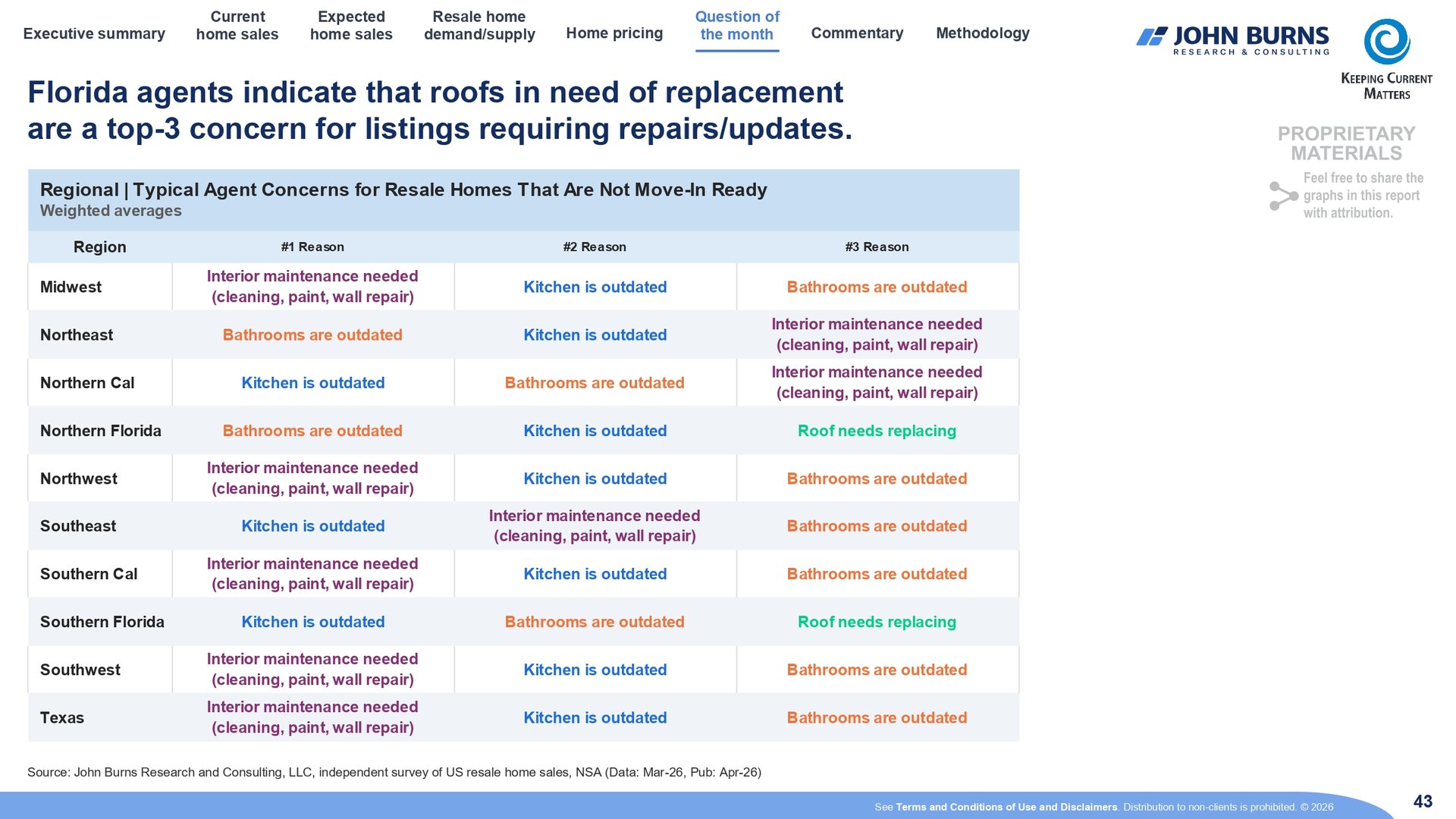

The John Burns survey specifically flagged that 71% of agents nationally cite outdated kitchens and interior maintenance as the top repair concerns for listings that aren't move-in ready. And in both Northern and Southern Florida, roof condition is a top-three concern, which is particularly relevant in the post-hurricane insurance environment we're navigating.

If you're preparing to list, reach out for a complimentary listing consultation. The difference between a strategic pricing approach and wishful thinking is measured in days on market and net proceeds, not in thousands, but often in tens of thousands.

The headwinds facing national real estate markets, affordability pressure, rate sensitivity, economic uncertainty, are real. But Sarasota's fundamental demand drivers are structural, not cyclical.

Buyers relocating from Illinois, New York, Michigan, and California aren't moving to Sarasota because of where mortgage rates are this month. They're moving because

For relocators from high-tax states, Florida's tax advantages alone often justify the move independent of any other consideration. The real estate market is the vehicle, not the destination.

The national real estate market is soft and uncertain. Sarasota's market is quietly rebalancing, with inventory falling sharply, sales volume rising, and forward-looking agent sentiment showing one of the strongest year-over-year improvements in the entire John Burns national survey.

This is not 2022. But it is also not the distressed market that national headlines might suggest.

If you're relocating from a high-tax state and considering Sarasota, the conditions right now favor buyers who are prepared to act thoughtfully. The window is open. How long it stays that way is the question.

Darren Dowling is the Broker-Owner of Beyond Realty LLC (The Dowling Group), a boutique luxury real estate brokerage specializing in Sarasota County, Manatee County, and the Gulf Coast barrier islands. Ranked in the Top 1.5% of brokerages nationwide, Beyond Realty holds a RealTrends "America's Best" designation and focuses exclusively on luxury residential real estate from $500K to $6M+.

Contact Darren: https://www.beyondrealtyfl.com/contact | Search Homes: https://www.beyondrealtyfl.com/search

YouTube: https://www.youtube.com/@The_Dowling_Group

DATA SOURCES:

Florida Realtors SunStats, Sarasota County Single-Family Homes, March 2026: https://sunstats.floridarealtors.org/

John Burns Real Estate Agent Survey, April 2026 (Data: March 2026): https://www.jbrec.com

This market analysis is for informational purposes only and does not constitute financial or investment advice. Real estate markets are local and conditions change. Contact a licensed real estate professional for guidance specific to your situation.

Beyond Realty LLC | 2170 Main Street, Suite 103, Sarasota, FL 34237 | beyondrealtyfl.com

Luxury Home Sellers Continue to Benefit from Strong Buyer Demand Across Sarasota, Manatee & Charlotte Counties

Single-Family Home Data from Florida Realtors® SunStats

Affordable Home Buying Opportunities in Sarasota, Lakewood Ranch, Manatee County, and Charlotte County

You’ve got questions and we can’t wait to answer them.